One of the most common crises small business owners face is the separation of personal vs business expenses. Especially when you're starting out as a sole proprietor, you may not immediately create a separate bank account or even apply for a business credit card. However, that's usually where the

Tackling Multi-Year Back Taxes: A Practical Survival Guide

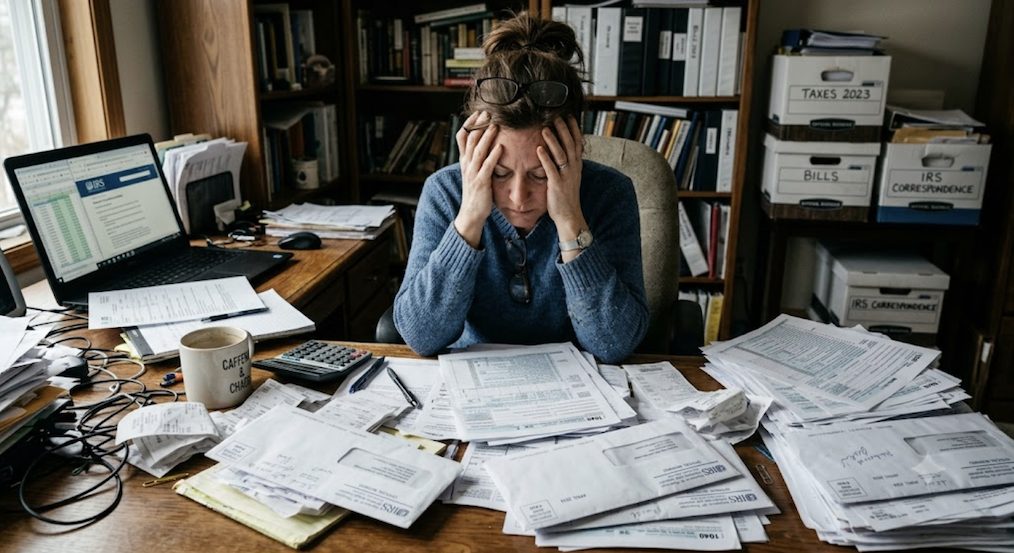

Discovering that you -- or your growing business -- owe three to five years of unfiled or unpaid back taxes is a daunting experience. The stress escalates rapidly when those liabilities span across state lines. Whether you are dealing with forgotten federal returns or complex multi-state reporting,

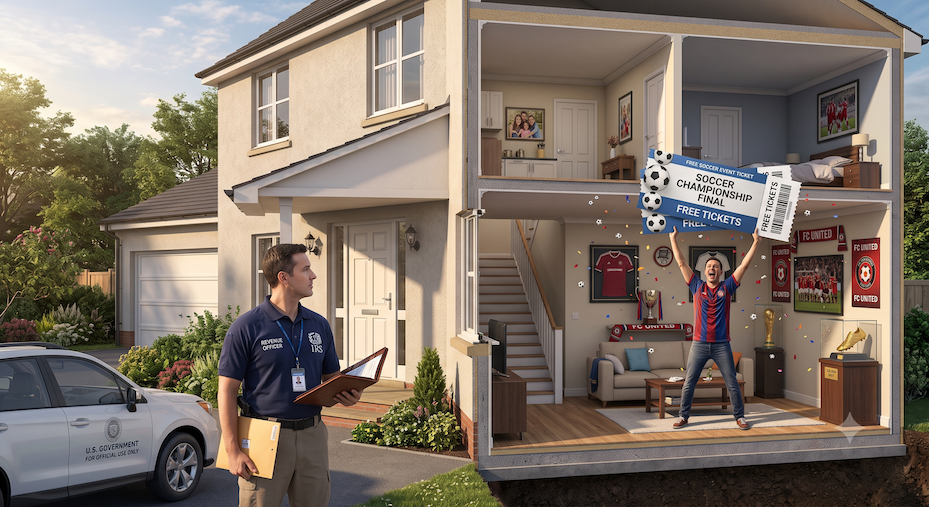

The Hidden Tax Traps of “Free” Tickets, Flights, and Client Perks

There's one golden rule of tax law: the IRS defines gross income broadly as any economic benefit realized, from whatever source derived. Winning a prize or receiving high-value perks from clients might feel like hitting the jackpot, but without proper planning, it can trigger an unexpected tax

From Refund to Balance Due: A Classic “Oops” of Amending a Tax Return

It is a great feeling: you finish pulling together your books, e-file your tax return, and the software tells you that you are owed a healthy refund. You breathe a sigh of relief and get back to running your business. But then, a few weeks later, the mailbox delivers a surprise -- a late Form

Cultivating an Urban Farm: Sowing Seeds for a New Business or Digging Into a Tax Trap?

For many homeowners and land investors in Washington State, the dream of self-sufficiency often blossoms into a business idea. Whether you own an empty multi-use lot or have a generous backyard in the Puget Sound region, turning an open plot of land into a micro-farm to sell fresh produce, herbs, or

Why Medical Practices Need a CPA on Speed Dial

Most businesses benefit from having a good accountant. Medical practices, however, often need one much more urgently than most other industries. Doctors, dentists, chiropractors, therapists, veterinarians, and other healthcare professionals operate in an environment where regulations change

Where to Park Your Cash if the AI Bubble Bursts

With the rapid acceleration of artificial intelligence across the Pacific Northwest tech corridor, a lot of capital has flown directly into high-valuation tech equities. But savvy business owners and investors know that rapid expansion can sometimes build a volatile market landscape. If you've been

How to Form an LLC Online: The Simplest Way to Start Your Business

Starting a business is exciting. Choosing a name, finding your first customers, and making your first dollar can feel like huge milestones. But before most entrepreneurs can officially operate, they need to decide how to structure their business. For many small business owners, freelancers,