If you’re involved in real estate through a partnership or S corporation, IRS Form 8825 (available for download here) is a key tax form you need to get familiar with. While it may not get as much attention as the 1040 or Schedule E, this form plays a major role in how your rental income is reported — and it can affect your bottom line.

Here’s a breakdown of what Form 8825 is, who needs to file it, and how to go about filling it out.

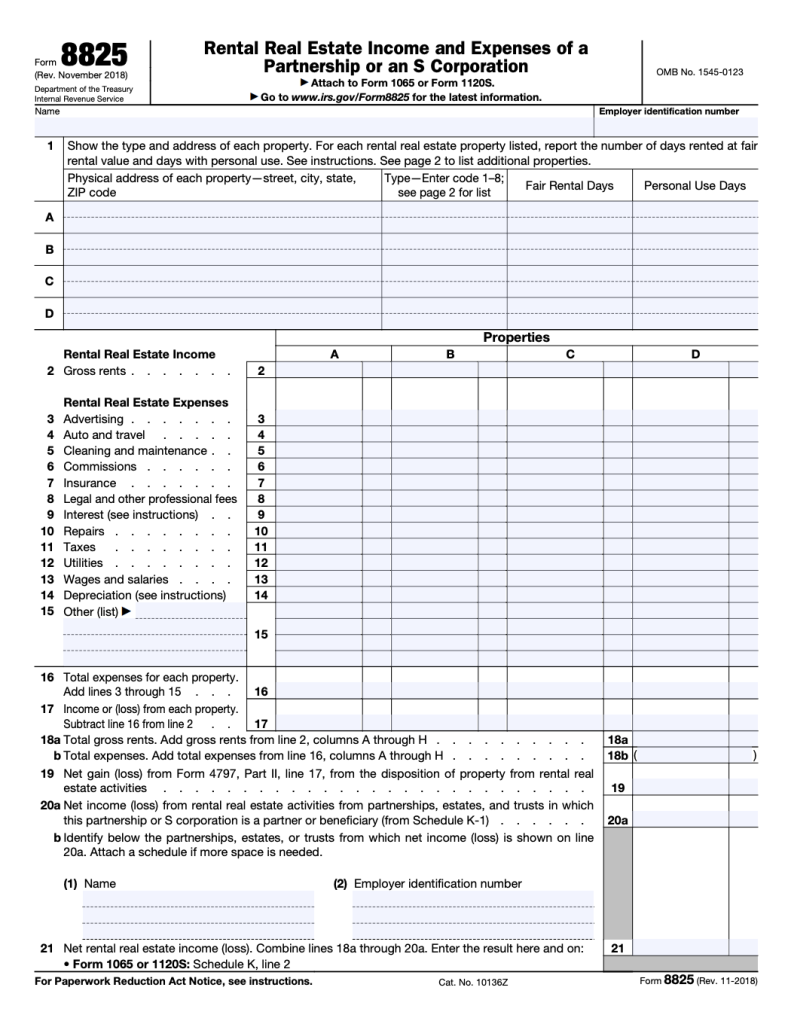

What Is Form 8825?

IRS Form 8825 is titled “Rental Real Estate Income and Expenses of a Partnership or an S Corporation” — really rolls off the tongue. This form is used to report the income, deductions, and expenses from rental real estate activities carried out through a partnership or S corporation.

Rather than using Schedule E (which is used by individuals), business entities use Form 8825 to report these activities as part of their informational tax returns (Form 1065 for partnerships or Form 1120S for S corps).

The goal? To determine the net gain or loss from rental property operations, which is then passed through to individual partners or shareholders to report on their personal tax returns.

Who Needs to File Form 8825?

You’ll need to file Form 8825 if:

- Your business is a partnership or an S corporation,

- You have ownership or participation in rental real estate, and

- That rental activity generates income or incurs expenses during the tax year.

This applies to landlords who own residential rental properties through an LLC taxed as a partnership or S corp, as well as real estate investment groups operating under a partnership model.

Most importantly, C corporations do not use Form 8825, nor do individual property owners (they typically use Schedule E).

Important Note: Do not use Form 8825 if you’re filing as a sole proprietor — in that case, you’d typically report rental income on Schedule E of your Form 1040.

C corporations also do not use Form 8825. Rental income would be reported directly on Form 1120.

If your entity owns multiple rental properties, each one should be listed separately on Form 8825.

The income or loss calculated on Form 8825 carries over to the appropriate lines on the parent return (Form 1065 or 1120S), and eventually to owners’ K-1s, where it may be subject to passive activity rules.

How to Fill Out Form 8825

Filling out Form 8825 requires accurate records of your rental income and expenses. Here’s a basic walkthrough of how to complete it:

1. Property Information

Start by listing each rental property separately. For each one, you’ll provide:

- Property address or description,

- Type of property (e.g., residential, commercial),

- Number of days rented and personal use (if any).

If you have multiple properties, the form has additional rows and allows attachments for more entries.

2. Rental Income

Report the gross rental income received from each property — this includes rent payments but not security deposits (unless retained due to lease breaches).

3. Expenses

Next, enter all deductible expenses associated with each rental property, including:

- Advertising

- Auto/travel (related to property management)

- Cleaning and maintenance

- Commissions

- Insurance

- Legal and professional fees

- Management fees

- Mortgage interest

- Repairs

- Property taxes

- Utilities

- Depreciation or depletion

These expenses should be directly tied to the rental activity, not personal use.

4. Totals and Net Income

At the bottom, you’ll calculate:

- Total income,

- Total expenses,

- Net gain or loss for each property.

This net number flows into the overall partnership or S corporation’s return and then into each partner’s/shareholder’s K-1, which they report on their personal taxes.

5. Passive Activity Rules

Keep in mind: most rental activities are considered passive unless you’re a real estate professional. This matters because passive losses can’t always be deducted against ordinary income — they may be limited or carried forward.

Pro Tips

- Keep detailed records of all rental income and expenses throughout the year.

- Don’t forget depreciation — it’s one of the most valuable deductions and is often overlooked.

- If your entity owns multiple rental properties, ensure each one is separately reported — mixing property data can raise IRS red flags.

- Consult a tax professional if you’re unsure whether your activity qualifies as passive or active, especially if you materially participate in property management.

Final Thoughts

Form 8825 might not be well known outside real estate circles, but for partnerships and S corps with rental activity, it’s essential. Filing it properly ensures you stay compliant with IRS regulations and maximize your allowable deductions.

Image generated by Sora.